Overview

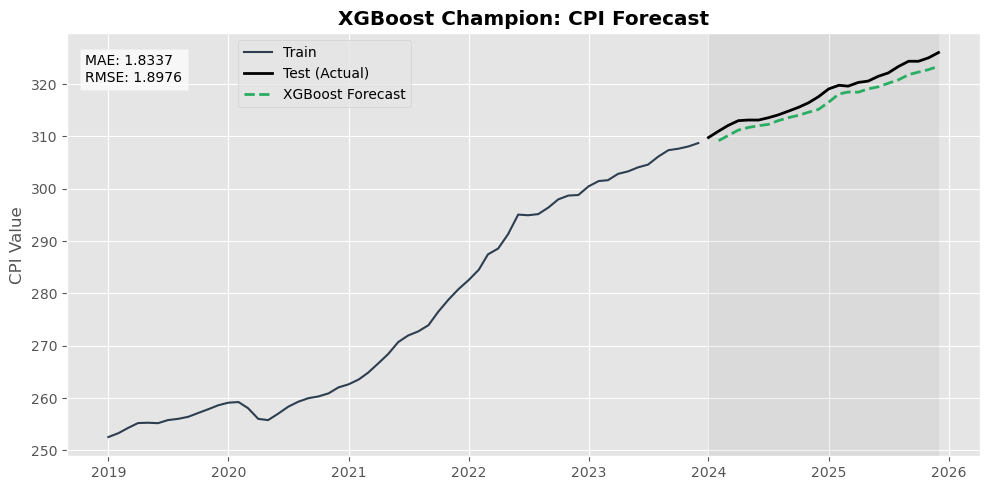

This project forecasts U.S. Consumer Price Index (CPI) values using a multi-model approach, ranging from classical statistical methods to gradient boosting. The primary objective was to evaluate model accuracy under a rigorous time-series validation framework and demonstrate production-level deployment on AWS SageMaker.

A key decision mid-project was pivoting away from LSTM after testing showed deep learning struggled with the small monthly sample size and non-stationary trend of CPI data — a deliberate architectural choice in favor of a more robust tree-based approach.

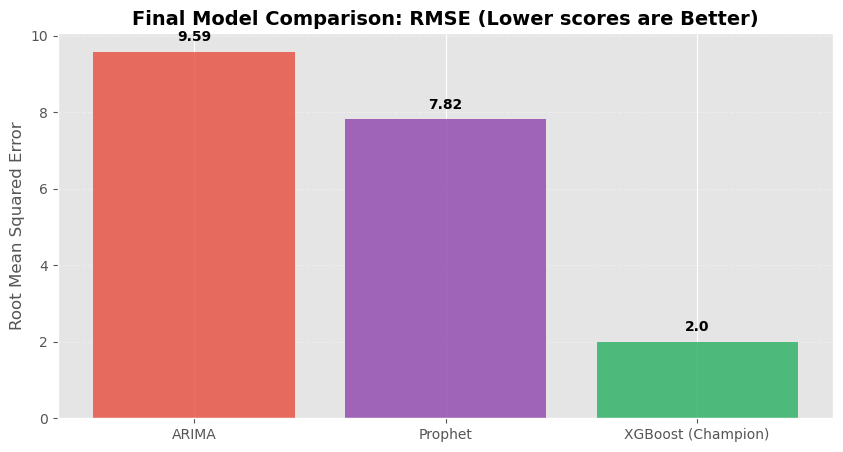

Results

Performance evaluated on a 24-month holdout set (Dec 2023 – Nov 2025):

| Model | MAE | RMSE |

|---|---|---|

| XGBoost (Winner) | 1.83 | 2.0 |

| Prophet | 7.09 | 7.15 |

| ARIMA (1,1,1) | 8.04 | 9.29 |

Data

- Source: Federal Reserve Economic Data (FRED)

- Series: CPIAUCSL (Monthly)

- Evaluation window: 24-month holdout

Technical Approach

- Applied first-order differencing to remove trend bias — model predicts monthly delta rather than absolute CPI values

- Engineered a 12-month sliding window of lag features to capture seasonal momentum and annual cycles

- Benchmarked ARIMA and Prophet as statistical baselines before training XGBoost

- Serialized the final model into

model.tar.gzwith a custom inference handler for SageMaker deployment - Deployment script intentionally separated from the notebook to avoid unnecessary cloud costs

Tech Stack

Python XGBoost ARIMA Prophet AWS SageMaker Boto3 Pandas Scikit-learn FRED API MLOps